Sunday, May 27, 2012

Last Post?

Well, it's been about two months since we posted to this blog. We did not intend to wait this long, but circumstances prevented us from posting. We really only had one other thing we had planned to possibly post. That was to create a more advanced version of the budget spreadsheet we discussed in earlier posts. However, we were unsure as to how many people would actually be interested in this. If you are one who is interested, please leave a comment saying so. If enough people express an interest, we'll prepare it and post it.

Also, if anyone has any questions about any of the previous posts in this blog, or if you just have general budgeting questions, please leave a comment with your questions.

For those who have followed this blog, we hope we have helped you with your household budgeting.

Thanks,

Randy and Kathy

Saturday, March 24, 2012

Wise Use of Credit Cards

As we have mentioned before, credit cards can be a good

thing, or they can be a bad thing. If you are one of those people who simply

cannot control your spending when you have plastic in hand, then cut up all

your cards and use checks, cash, or debit cards. This will limit your spending

to what you actually have in the bank. You can still get in trouble if you

spend all your money on frivolous stuff, leaving no money for essentials later.

But at least you will be somewhat limited on the amount of debt you accrue.

If, on the other hand, you have a handle on spending, credit

cards can be very useful. First off, they allow you to easily pay for things

without having to immediately deduct money from your bank account. If you pay

off the credit card bill each month in a timely manner, it basically amounts to

an interest-free short-term loan. But if you plan to build up a balance on a

card and then pay only a portion of it each month along with interest payments,

then forget about using credit cards. The interest on credit cards can be

pretty steep. You don’t want to get stuck making these hefty payments if at all

possible.

Here’s what we personally look for in credit cards. REWARDS!!

A card must not have an annual fee, unless

the rewards paid by the card more than compensate us during the year.

Currently, all the cards we own have no annual fees. Also, the card must allow

us to pay it off in full each month with no interest or penalties. In other words,

the cost to us for the card’s use must be zero, but additionally it must pay us

back. In essence, the credit card company should be paying us for using their

card. Another feature to look for is the ability to have the credit card company

automatically withdraw the total amount due from your bank account each month.

This prevents you from accidentally being late making a payment, resulting in

interest and late fees. Just make sure you have enough money in your bank

account to cover the withdrawal when the bill comes due. We set up monthly

reminders on our electronic calendar for this purpose.

Some cards pay back a percentage of each purchase regardless

of where the purchase is made. Other cards give rewards based on the type of

purchase. Common ones are for gas stations, grocery stores, and drug stores. If

you travel a lot, some cards give rewards that can be used for airline flights.

Also, some businesses team up with Visa or MasterCard to provide a card with

rewards, particularly if you use the card at the business. Some businesses have

their own credit cards that can only be used at their stores.

If you look around, you can find some pretty good deals on

cards. Here are a few we use that you might want to look at. Please be aware

that the description of the rewards we receive with these cards can change at

any time. In fact, we have occasionally quit using cards when they change their

rewards programs to be less desirable or when better cards come along to

supplant them.

This is a good general use card because it pays a flat 2%

cash back on all purchases. In order

to get this card you will have to set up a Fidelity Investments account. The

rewards can be deposited into either a taxable account, an IRA, a college

savings plan, or sent to the cardholder as a check. However, the full 2% is

only available in check form if we let the rewards build up to at least $250.

We use this card for all purchases except for those where we get a bigger

reward using another card. The one disadvantage of this card is that quite a

few businesses, especially small local ones, do not accept American Express

cards due to their higher merchant fees.

This card is issued from the Pentagon Federal Credit Union. This

account is primarily designed for government, particularly military, personnel.

However, we were able to make a donation to an organization that supports

military families, and that allowed us to join. You must also set up a savings

account with the credit union and make at least a $5 deposit. However, the

rewards are well worth it. You get 5% back on pay-at-the-pump gas purchases, 3%

on supermarket purchases, and 1% elsewhere. We only use this card at gas

stations, supermarkets, and any place that does not accept American Express. Gas

companies, such as Shell and BP, sometimes offer credit cards that have 5%

rewards on purchases made at their stations, but we much prefer having one card

that gives us 5% back for gas purchased anywhere.

Normally the rewards paid by the Discover card are not as

large as those from some other cards. However, every few months, special 5%

bonuses are offered on certain purchases. For instance, it will soon be

offering 5% cashback bonuses at restaurants and movies. One caveat is these

specials always have spending caps. We only use Discover when the special

offers are better than what we can get with any other card. Points earned with

the Discover card have to be redeemed with gift cards. Some cards can be

purchased for less than their face value. One of our favorite ways to cash in

our Discover points is to get a $50 Chili’s Grill & Bar gift card in

exchange for $45 in points.

Some businesses offer credit cards that give you substantial

rewards for use at their store. For instance, the Best Buy RewardZone

MasterCard offers a 4% reward for purchases made at Best Buy and 1% elsewhere.

Amazon’s Visa card offers 3% rewards for Amazon purchases, 2% for certain types

of other businesses, and 1% elsewhere. Many times the rewards come as vouchers

that can be used at their store rather than as cash. However, if you make

regular purchases at these stores, that’s as good as cash.

Store Cards

Some stores, such as Kohl’s, JCPenney, Sears, and others,

offer credit cards that can only be used in their respective stores. Under

normal circumstances, these cards generally don’t offer any incentives for

their use. However, occasionally the stores will offer sales that can only be

taken advantage of when using their card. It can be very useful under those

circumstances, especially given that they usually give the discount at the time

of purchase. Still, we do not bother with a card from a store we shop at

infrequently. Oftentimes a store will offer a steep discount on the entire current

purchase for opening a credit card account with them. We sometimes do this if

we are making a large purchase and the discount is substantial, but normally we

take a pass on these offers.

Student Cards

Some credit card companies offer cards that are geared

toward college students. They will typically offer rewards on purchases that

are of interest to this age group. Our son uses the Citi

Forward Card. It should go without saying, but we’ll say it anyway. If your

college-age child is not very responsible with their spending, DON’T give them

a credit card. BAD IDEA!

There are many, many different types of credit cards on the

market to meet the needs of essentially every type of spender. We have

mentioned only a few that we have found to be useful. For others, check out the Credit Card

Guide.

Keep in mind that the deals can change frequently. The

rewards we mentioned earlier may not be available by the time you read this. Also,

there may be cards available that we would like better, but just haven’t

happened onto them yet. Indeed, if anyone reading this finds a great credit

card, be sure to let us know about it.

If you use credit cards at a lot of different businesses, you

may find that to maximize your rewards, you may need to have a plethora of

different cards. This can become unwieldy. Sometimes you just have to say, “No

more cards.” Decide how many cards you are willing to keep up with, determine

which ones will benefit you the most, and go with just those. If you

occasionally order merchandise from Internet sites that you are not totally

confident in, you will want to have one credit card with a low spending limit

so nefarious individuals who might decide to use the card will be limited on

what they can spend.

Speaking of credit card theft, be sure to find out if you

are responsible for some amount of money should a card be lost or stolen and

then used by someone else. If seems to us that most companies’ cards these days

do not require a fee from you under these circumstances. Another thing to be

aware of is that some cards cap their rewards. This is okay. Just remember to

switch to a different card once you reach that cap because you will no longer

receive any rewards on purchases that exceed the cap. And again, watch out for

those annual fees and penalties.

Happy credit card shopping. May your balances be paid in

full each and every month.

Wednesday, March 7, 2012

Cutting Expenses Part 2

An area where cuts can help a lot with your bottom line is

utilities, primarily heating and cooling. Of course, the cost of utilities vary

greatly depending on where you live, both because of the climate and the cost

of power. The latter varies greatly with the source of power. Several years ago

the cost of natural gas became extremely high and people who used it were

wishing they could heat with electricity. Now, natural gas prices are down, and

the reverse is true. But apart from the type of energy you use for heating and

cooling, the only real way to control its usage, assuming your house is

insulated properly, is to lower the thermostat in the winter and raise it in

the summer. (And by lowering and raising, we do not mean moving it close to the

floor in the winter and near the ceiling in the summer.) We know this can be

difficult, especially for older people. We used to keep our house at about 70

deg in the winter, but as we aged, this became unacceptable. So, now we keep it

at 73 deg. Right now we can afford that, but should prices rise, we may have to

resort to using space heaters just in the part of the house we are currently in

or bundling up more. We have always kept the house at 78 deg in the summer, but

Randy has to supplement with fans to be comfortable as he is more warm natured

than Kathy. Anyway, in your case, you just have to find a balance between

comfort and your checking account.

Other big power users are stoves, ovens, and clothes dryers.

So, if you can limit the usage of stoves and ovens for cooking, you can save

money. But if you make the alternative to eat out, then you’ve just shifted a

few dollars in savings on utilities to a lot of dollars of non-savings on food.

One thing we do is to use a toaster oven for smaller items rather than heating

up the big oven. If push comes to shove, the clothes dryer can be eliminated

altogether by using the old fashioned method of drying: hanging on a clothes

line in the back yard. This may not be feasible when the weather is bad, but we

can remember as a child having clothes hanging on racks around the house when

it was raining. And we can also remember having ice on our clothes when they

were hung outside and the weather turned cold unexpectedly. The point is: use

your best judgment about when to use certain types of energy. If your budget is

tight, these are the types of decisions that must be made on a daily basis.

Little things you can do include: turning off lights and

devices when not being used, letting sunlight into the house in the winter and

blocking it in the summer, putting insulation on your hot water heater, using

fluorescent bulbs rather than incandescent, taking fewer hot showers in the

winter, and hand-washing dishes rather than using a dish washer. In general,

just become more aware of how you are using energy around the house and cut

where possible.

Another area for a large potential in savings is

communications. Are you paying for a landline phone service? Cell phone

service? TV service? Internet service? Pager service? There are so many

communication services available, it can eat up a lot of money. When it’s all

said and done, you could eliminate all these services and still live well. It

wasn’t that long ago that many of these services didn’t even exist. We know

that in our modern society these things all seem essential, but in reality they

are simply just desirable. Even if you decide you don’t want to rid yourself of

any of these conveniences, there are ways to lower your cost.

Consolidate. If you have landline phone service with one

company, cell phone service with another, and Internet service with yet

another, then you can most likely save quite a bit of money by consolidating

these services with one company. We just recently rolled our landline phone,

TV, and Internet service into a bundle with one company. We will save about $80

per month for the first year and about $40 per month from then on. If you

really don’t want to change service, we have heard about other people talking

to the companies they currently have service with and asking for a good

customer discount. Many times they will give you the same price they offer to

first time customers for a year. If asking doesn’t work, you can tell them you

are planning to switch your service to another company unless they can give you

a better price. Although we still like having a landline phone, we have a lot

of friends and family that have dropped this and converted totally to cell

service. This can save you money for sure, especially if you bundle the cell

service with TV and Internet service.

Another great money drainer is transportation costs. The

current high cost of gasoline is driving much of that. However, if you have a

proclivity for new expensive cars, most of your problem may be high car

payments. If you are on a tight budget, you have no business buying expensive

cars. Go for the lower cost vehicles that get high gas mileage. If you can find

a decent used one, then you can save even more.

Buying used is what Dave Ramsey recommends, but we

personally like buying new vehicles and driving them until they break down and

are too expensive to repair and maintain. However, we do invest in having our

vehicles serviced regularly, believing that this will prolong the life of the

vehicles and thus save us money over the long run. But that’s us. We have a

relatively decent income and have been able to afford new cars when needed.

However, our son owns a used car and it has served him well now for several

years. If our income were lower and we were in need of a vehicle, we wouldn’t

hesitate buying used. Also, if you have the skill and the time, you might want

to do some of the servicing yourself to save money.

If you live a long distance from your job, you seriously

need to think about carpooling to save money. We know this can be inconvenient,

but if saving money is your goal, it will be well worth it. If you use public

transportation, you might consider riding a bicycle or even walking, if

possible and the weather permits.

Be creative. Record how you are spending your money and put

together a plan on how to reduce that amount. You must begin to be totally

honest with yourself about what is really needed

and what is merely wanted. Thinking

that something is needed rather than simply wanted leads many people to

becoming impulse buyers. They’ll go to the store to pick up a few needed items and leave the store with

three times as many wanted items as needed items. This is not good. But some

people have a bad habit, or even a compulsion, to rationalize to themselves

that a wanted thing is really a needed thing. Like, “I really need an iPad. It’s so much easier to

play solitaire while riding down the road than using cards. And I can check my

Email without having to get on my computer.” Come on now. That’s not a valid

reason. Unless you need an iPad to do your job, then it remains a luxury item

for those that want it and can afford it. If you don’t have the money, let the

iPad remain at the store. Then have a long discussion with yourself. Conduct an

intervention if you will. On YOURSELF. Tell yourself, “I don’t really need all

this stuff, I just want it. So, get over it, self! Quit borrowing money to

support my spending habits. I’ll be glad I did.” Once you have these ideas

firmly planted inside your head, you will find that you really can leave those

wanted items on the store shelf. If you find that you cannot, then you may need

to seek professional help.

So, let’s stop here. We hope you take these suggestions to

heart and that it helps you to live within the budget your income allows.

Wednesday, February 29, 2012

Cutting Expenses

One thing that can destroy relationships quickly is the

mishandling of finances. Soon after marrying my wife almost 30 years ago, she

told me she wanted us to start a budget. She had heard that one of the most

frequent things couples argued about and got divorced over was money. Although

I was a bit skeptical, she soon persuaded me that we should have a budget. In

those days, home computers were expensive and rarely seen. So our first budget

was done using a ledger book. Later, when the Commodore 64 became widely

available, we bought one and began keeping our budget in a spreadsheet. This

made budgeting much easier and less prone to errors.

Now, after nearly 30 years, we still keep a budget and very

much believe in them. It has helped keep us on the straight and narrow when it

comes to spending our hard-earned dollars. However, creating a budget is easy;

living by it is another matter. For those of you fortunate enough to have

relatively good salaries, sticking to a budget may not be difficult at all.

However, for those that struggle daily with having enough money to live on,

living by a budget may be extremely difficult. For that reason, we now present

some ideas on how to cut your household expenditures.

First and foremost, whatever you do, DO NOT look to the

federal government for an example of how to run your household. Our leaders

have gone bonkers over the last 50 years and are about to drive our entire

country into bankruptcy. Did you know that our national debt has now exceeded

$15 trillion and that it is projected to increase by about $1.1 trillion in

fiscal year 2012 alone. Because of this debt, we spend almost $500 billion a

year in interest. Yet, revenues are only expected to be about $2.6 trillion.

Let’s scale these numbers down to the average household in the US and see what

they look like.

Household income:

$50,000

Total existing debt:

$288,462

Additional debt for 2012:

$21,154

Interest to pay in 2012:

$9,615

Can you imagine being in a situation where you are spending

almost 20% of your income just to cover the interest on your debt? Perhaps you

can. If you are young and just getting started on your career, you could be in

debt this much because of a mortgage and car loans. But keep in mind these are

loans you are working to pay off without incurring additional debt (unless you

are going wild with the credit cards). But what if you only paid the interest

on your debt, never paying anything on the principle. Then, on top of that, you

buy new $20,000 cars every year and start making interest payments on them

also. This is what the federal government is essentially doing. It is

completely unsustainable. The party has to end at some point, hopefully without

too much of a hangover. Therefore, we have decided to help you cut your

spending should you find yourself in a situation where this is necessary.

The first thing to think about is the absolute essentials of

life. These are normally considered to be food and shelter.

Yes, you need a dwelling place. But do you need one as

expensive as the one you have? If you

find yourself hating that dream home you own because the cost of the mortgage,

taxes, insurance, and upkeep are eating into your lifestyle, it may be time for

a change. We like having a DREAM LIFE more than having a DREAM HOME. Of course,

it may still be difficult to part with the home, so the first thing to do is to

see if you can reduce the mortgage payments by refinancing. You have to be

careful here because closing costs can be so high as to negate any benefits of

a lower interest. Also, you may find yourself in a situation where the value of

your home is less than the amount you owe. But if the overall housing market is

depressed in your area, it could still be feasible to greatly reduce your cost

of home ownership by selling your existing home at a loss and buying a much

lower cost home. Because there are so many factors affecting cost, it is a good

idea to consult with a real estate professional about your options.

I have mentioned the cost of food in previous posts. This is

the one area that our family tends to have the most problems since we enjoy

eating out so much. One of the reasons we shy away from home meals is the time

it takes to prepare them and clean up afterwards. We have a fairly busy

lifestyle and don’t like taking that big a chunk out of our leisure time. Sure,

we could just heat up a can of soup, but we like variety. Some foods simply

take time to prepare.

One thing that helps us to eat at home more is planning a

week in advance what we will have each night. This allows us to purchase what

we are lacking ahead of time and have everything ready to go each evening

rather than having to make a run to the grocery store on the spur of the

moment. Also, we can plan easier meals for busy nights and more elaborate meals

for free nights. If, however, you are on a really tight food budget, planning

ahead will be only one step in your savings plan. You may also have to greatly

cut back on more expensive food items such as steak, or at least concentrate on

the cheaper cuts. We have discovered that even fresh fruit can be expensive

because many times the fruit is not good or it spoils before we have time to

finish it. Canned and frozen items are better choices for longer term storage.

You might want to start couponing. It’s also a good idea to

look for deals on more expensive food items that can be frozen. We buy a large

quantity of meat when on sale, vacuum seal it, and put it in the freezer. But

if push comes to shove, you may regrettably have to cut out eating some foods

that you really like. Better that than going broke.

Another area that can be problematic is the purchasing of

technology items. Just look around. Big screen TVs (now with 3D!), stereos,

Blu-ray players, cable service, satellite service, computers, laptops,

printers, tablets, wireless phones, cell phones, iPods, iMacs, iPhones, iPads,

iThis, and iThat. Temptation is all about. Our household consists of tech

geeks, liking all these new gadgets. Yet, when you think about it, are they

really necessary. No, they are not!

If you find yourself spending thousands of dollars you do not have on

technology, STOP IT! This is an intervention. Look seriously at what you are

spending on these items and scale back to only what your budget allows. You

might also consider selling some of your existing stuff on eBay. We’ve got a

Nintendo Wii and accessories waiting to be sold right now. Anyone interested?

Only those who can afford it need apply.

Look for more savings tips in the next post.

Monday, January 30, 2012

Second Budget

Well, hopefully you made it through setting up your real budget just fine and were able to get all your transactions entered for the first half of the month. It’s now time to examine how your second budget might look. Remember that the Savings column can look either better or worse than it really is after the first budget. It depends on when your paychecks come in. If all paychecks are received twice a month or perhaps every two weeks, then the Savings numbers should reflect reality. However, if one or more paychecks are received only once a month, then the numbers can look good or bad depending on what time of the month they are received. In the case of our sample budget for Jack and Jill, Jill receives two paychecks per month while Jack gets one during the first two weeks of each month. This made their Savings category look really flush with money on the first budget. But as you can see below, the second budget brings the Savings back in line (with a balance of over $300) because Jack has no paycheck being deposited during this budget cycle.

Click image for an enlarged view

Click image for an enlarged view

Download OpenOffice Calc version of this spreadsheet

Download Microsoft Excel version of this spreadsheet

As you can also see, some other regular bills were paid during this half-month cycle. Fortunately, most budget categories held their own. However, it appears that an unexpected plumbing problem cost Jack and Jill $85 and thus put their House Upkeep category in the red. This is okay as long as no other unexpected repairs are needed in the near future. If the overall balance in their checking account remains above zero, then there is no need to panic. Hopefully, the deficit in any given categories can be made up over the next few budget cycles.

The only other possible problem seems to be in Jack’s personal money column. He’s in the red by almost $16. If Jack has at least $16 in his wallet, he is okay; but if not, he needs to watch what he spends over the next budget cycle to make up the deficit.

Notice that Jack and Jill did real well with their Food budget. They ended the month with a surplus of $34. As long as they can maintain this level of spending, all will be well. However, if they begin to loosen up too much and start eating out more, they could find themselves in trouble.

If you found yourselves, in your real budgets, overspending left and right, then all we say is that you must begin changing your mindset right now! We know it can be difficult going from freely spending money to spending a controlled amount. You must begin settling for less. It can be done. Many other people have done it. As you work towards your goal of reducing spending, one thing to keep in mind is that most of what we buy are things we want rather than things we need. If you were to cut your spending to just your needs, you would most likely find yourself spending much less than you are taking in. So, whenever you find yourself wanting to make a purchase, evaluate the necessity of the item and how the purchase will affect your budget’s bottom line. If it’s not really needed and your budget can’t handle it, don’t buy. Keep working at this until the lower spending amounts just come natural to you.

In the next post, we’ll give you a few tips about controlling spending in case you continue to have problems.

Download OpenOffice Calc version of this spreadsheet

Download Microsoft Excel version of this spreadsheet

As you can also see, some other regular bills were paid during this half-month cycle. Fortunately, most budget categories held their own. However, it appears that an unexpected plumbing problem cost Jack and Jill $85 and thus put their House Upkeep category in the red. This is okay as long as no other unexpected repairs are needed in the near future. If the overall balance in their checking account remains above zero, then there is no need to panic. Hopefully, the deficit in any given categories can be made up over the next few budget cycles.

The only other possible problem seems to be in Jack’s personal money column. He’s in the red by almost $16. If Jack has at least $16 in his wallet, he is okay; but if not, he needs to watch what he spends over the next budget cycle to make up the deficit.

Notice that Jack and Jill did real well with their Food budget. They ended the month with a surplus of $34. As long as they can maintain this level of spending, all will be well. However, if they begin to loosen up too much and start eating out more, they could find themselves in trouble.

If you found yourselves, in your real budgets, overspending left and right, then all we say is that you must begin changing your mindset right now! We know it can be difficult going from freely spending money to spending a controlled amount. You must begin settling for less. It can be done. Many other people have done it. As you work towards your goal of reducing spending, one thing to keep in mind is that most of what we buy are things we want rather than things we need. If you were to cut your spending to just your needs, you would most likely find yourself spending much less than you are taking in. So, whenever you find yourself wanting to make a purchase, evaluate the necessity of the item and how the purchase will affect your budget’s bottom line. If it’s not really needed and your budget can’t handle it, don’t buy. Keep working at this until the lower spending amounts just come natural to you.

In the next post, we’ll give you a few tips about controlling spending in case you continue to have problems.

Saturday, January 14, 2012

First Budget

Alright, it’s time for the action to begin. Let’s put some transactions for the first half of the month on the initialized spreadsheet. We have put together a sample budget to show you what it might look like. Yours will probably look much different, but the elements should be similar. Here’s a screenshot of our sample budget. (Click on the screenshot for a larger image.)

Download OpenOffice Version

Download OpenOffice Version

Download Excel Version

Looking down the left columns you will see that the transactions have been divided into three general groupings. The first group is for direct transactions. The second is for credit transactions. The third is for cash transactions. Let’s look at these groupings in more detail.

Direct Transactions

Direct transactions are those that affect your checking account directly and include such things as checks, a debit card, online Bill Pay, automatic deductions, withdrawals, deposits, and so on. The sample budget shows a number of these. The Trans Number column is used to distinguish between them. For instance, when checks are written, the check number is entered. When an automatic payment is made, “AutoPay” is entered. Deposits and withdrawals are designated with abbreviations “DEP” and “WDL”. No debit transactions are shown, but we normally use “DEB” to indicate it on the budget. If you have Bill Pay available on your account, you can easily make payments to many different institutions via online transactions. Typically, a confirmation number is automatically generated when a Bill Pay transaction is finalized. We use “BP-” followed by this confirmation number to designate a Bill Pay transaction on our budget.

The sample budget has 10 direct transactions. Three checks (numbered 1103, 1104, and 1105) were written. Jack and Jill have automatic payments set up for their mortgage and their utility bills. Two Bill Pay transactions occurred. One was for a MasterCard payment, and the other one for a phone and internet bill with AT&T. Jill also made a direct withdrawal in order to have a sufficient amount of cash in her purse. And now the good news. Jack’s monthly paycheck was deposited as was Jill’s semimonthly paycheck.

Notice that when a payment or withdrawal occurs, the amount is subtracted directly from the column(s) designated for those type of payments. The AT&T bill was paid directly from the Communications category, the utility bill directly from the Utilities category, and so on. When Jill withdrew money to have cash in her wallet, the amount was subtracted from Jill’s column. We will discuss handling cash in more detail later.

Since we already have semimonthly allowances built into the spreadsheet, all paycheck deposits go directly into the Savings column. In Jack and Jill’s case, Jack receives a paycheck at the beginning of every month while Jill receives two checks each month, one in the middle of the month, the other at the end. So, don’t be deceived into thinking Jack and Jill have lots of money in Savings. They do at this time, but remember that only Jill will be receiving a paycheck during the next budget cycle. Each budget cycle requires subtracting $1943 from Savings for allocating to all the budget categories. So, the amount that will be in Savings at the end of the next budget cycle will be $1391.33 (current balance) - $1943 (for allocations) + $857.33 (Jill’s paycheck). This totals to $305.66. This better represents the true amount of Savings that Jack and Jill have.

Credit Transactions

When you make a purchase with a credit card, you are not directly affecting your checking account. Rather, you are simply building up a balance with the credit card company that will have to be paid at a future date. Yet, you still need to account for the spent money on your budget. For this reason, whenever a credit card transaction occurs, money needs to be subtracted from the appropriate budget columns. An equal amount of money then needs to be added to the Credit Card category. This methodology insures that you will have enough money available when the credit card bill comes due, allowing you to pay it off in full each month.

The sample budget indicates that Jack and Jill had 11 credit card purchases during the first half of the month. Notice that in some cases one transaction can result in deductions from multiple columns. For instance, Jack bought $72.50 worth of food at WalMart, but also bought a magazine for $5.28. The latter is a personal item and thus is subtracted from Jack’s budget category. Of course, the amount of the total purchase, $77.78, gets added into the Credit Card column. A similar split occurs for the family’s outing to the movie theater. Based on the low cost of the tickets, it appears that they went to a matinee.

Remember that Jack and Jill are also putting an extra $250 every budget cycle into the Credit Card category in order to have extra money to pay off existing debt. Thus, when a credit card bill comes due, their total payment will be the amount of all the purchases made during the billing cycle PLUS the amount designated for paying off their existing debt. Let’s suppose that $100 was allocated for paying off their existing MasterCard debt. Further suppose that $400 in charges were made during a billing cycle. Then, the payment for that cycle will be $500.

Cash Transactions

All the money carried in an individual’s wallet should be thought of as being that person’s personal money. Therefore, if Jack pays cash for something personal, such as a book, then nothing needs to be put on the budget spreadsheet. However, if Jack pays for a snack with his cash, then he will need to be compensated for this on the budget by transferring the cost of the snack from the Food category to the Jack category. This means it is a good idea to make a note of any non-personal cash transactions to help you remember to compensate yourself on the next budget.

Since this is your first budget, you may not want to start out having a personal claim on the money in your wallets. You may have different amounts and it wouldn’t be fair starting out with one person having more money than the other. So, let’s just say that any money in your wallets at the beginning of the month is money that belongs in Savings. There is no need to actually deposit this cash into your checking account. You can simply transfer money on the spreadsheet. For our sample budget, Jack started the month with $100 in his wallet while Jill started with $25. The “Initial Cash Balancing” entry on the spreadsheet handles the compensation by transferring $100 from Jack’s column and $25 from Jill’s column to the Savings column. After doing this, all the cash in their wallets can now be considered their personal money.

How Did They Do?

So, how did Jack and Jill do? Quite well, actually. They managed to keep most of their budget categories in the black. You might thing they messed up by overspending on food. Perhaps, but another explanation could be they bought enough food this budget cycle to last through much of the next one. If this is so, we can expect them to spend less on food during the next budget cycle. However, if they did truly overspend, then they will just have to hunker down and spend less during the next budget cycle.

It also appears that both Jack and Jill severely overspent their personal money. Not so. Remember that they both started with some cash in their wallets and Jill also made a cash withdrawal. So, if Jack started with $100 in his wallet and spent only $22 for personal stuff, he would still have $78 left. He also spent $2 for a snack, leaving him with $76, but keep in mind this was reimbursed to Jack on the budget from the Food category. So, if Jack has $76 in his wallet and his budget column is left with a deficit of $59.28, he still has a net amount of $16.72 ($76 - $59.28). So, Jack is good. Jill started with $25 and withdrew an additional $40 from the bank. This gave her a total of $65. Of that, she spent $5.46 on food, $4.50 on miscellaneous items, and gave $20 in cash to charity. Of course she was reimbursed these amounts on the budget, but that still left her with less cash. $35.04 to be exact. If she spent $9.50 on personal items, she would be left with $25.54. Subtracting her budget deficit of $23.72, Jill ends up with an overall balance of $1.82. Above zero, but not quite as good as Jack’s overall balance of $16.72.

Finishing Up

Once the budget spreadsheet is complete, we recommend saving it with a filename of Budget-YYYY-##, where YYYY is the current year and ## is the budget number for that year. So, for this first budget of the year, the name would be Budget-2012-01. As more budget spreadsheets are created during the year, the last two digits will increase by one for each new budget. If you want to keep a hardcopy record of your budget sheets, then print this spreadsheet.

Once you have saved this file as Budget-2012-01, you need to prepare the sheet to accept the transactions for the next budget cycle. There are several steps you need to take.

1. Since the Ending Balance for this cycle is the Starting Balance for the next, you need to copy and paste the Ending Balance numbers to the row showing the Starting Balance. So, select cells D80 through U80, select menu item Edit/Copy, select cell D3, and then select menu item Edit/Paste Special, choosing Numbers as the method to paste. The Paste Special option is needed because the Ending Balance cells are actually formulas that add together all the cells above them. By performing a Paste Special – Numbers, the numerical results of the formulas are pasted into the Beginning Balance cells rather than the formulas themselves. Upon selecting the menu item Edit/Paste Special, OpenOffice Calc shows the following dialog box:

Excel presents something similar. In either case, the important point is that the Numbers option is the only thing selected.

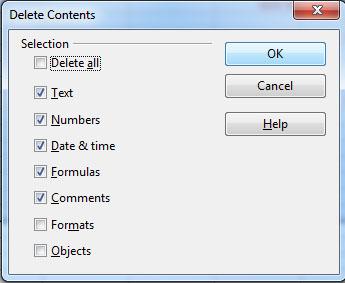

2. All of the transactions for this first budget cycle need to be deleted to make way for the second budget cycle transactions. Select cells A4 through U78 and press the Delete key on your keyboard. OpenOffice Calc will show the following dialog box:

You want to delete all the content of these cells, but not the formatting since that will rid the cells of their Currency formatting.

3. Finally, you need to modify three cells. First, change cell A1 from 2012-01 to 2012-02. Next change the Starting Balance date to Jan 15 and the Ending Balance date to Jan 31. Now the sheet is ready to accept transactions for the next budget cycle and can be saved with a filename of Budget-2012-02. Here’s what it should look like.

Download OpenOffice Version

Download OpenOffice Version

Download Excel Version

In the next post, we’ll create some more sample transactions for the second budget cycle.

Download Excel Version

Looking down the left columns you will see that the transactions have been divided into three general groupings. The first group is for direct transactions. The second is for credit transactions. The third is for cash transactions. Let’s look at these groupings in more detail.

Direct Transactions

Direct transactions are those that affect your checking account directly and include such things as checks, a debit card, online Bill Pay, automatic deductions, withdrawals, deposits, and so on. The sample budget shows a number of these. The Trans Number column is used to distinguish between them. For instance, when checks are written, the check number is entered. When an automatic payment is made, “AutoPay” is entered. Deposits and withdrawals are designated with abbreviations “DEP” and “WDL”. No debit transactions are shown, but we normally use “DEB” to indicate it on the budget. If you have Bill Pay available on your account, you can easily make payments to many different institutions via online transactions. Typically, a confirmation number is automatically generated when a Bill Pay transaction is finalized. We use “BP-” followed by this confirmation number to designate a Bill Pay transaction on our budget.

The sample budget has 10 direct transactions. Three checks (numbered 1103, 1104, and 1105) were written. Jack and Jill have automatic payments set up for their mortgage and their utility bills. Two Bill Pay transactions occurred. One was for a MasterCard payment, and the other one for a phone and internet bill with AT&T. Jill also made a direct withdrawal in order to have a sufficient amount of cash in her purse. And now the good news. Jack’s monthly paycheck was deposited as was Jill’s semimonthly paycheck.

Notice that when a payment or withdrawal occurs, the amount is subtracted directly from the column(s) designated for those type of payments. The AT&T bill was paid directly from the Communications category, the utility bill directly from the Utilities category, and so on. When Jill withdrew money to have cash in her wallet, the amount was subtracted from Jill’s column. We will discuss handling cash in more detail later.

Since we already have semimonthly allowances built into the spreadsheet, all paycheck deposits go directly into the Savings column. In Jack and Jill’s case, Jack receives a paycheck at the beginning of every month while Jill receives two checks each month, one in the middle of the month, the other at the end. So, don’t be deceived into thinking Jack and Jill have lots of money in Savings. They do at this time, but remember that only Jill will be receiving a paycheck during the next budget cycle. Each budget cycle requires subtracting $1943 from Savings for allocating to all the budget categories. So, the amount that will be in Savings at the end of the next budget cycle will be $1391.33 (current balance) - $1943 (for allocations) + $857.33 (Jill’s paycheck). This totals to $305.66. This better represents the true amount of Savings that Jack and Jill have.

Credit Transactions

When you make a purchase with a credit card, you are not directly affecting your checking account. Rather, you are simply building up a balance with the credit card company that will have to be paid at a future date. Yet, you still need to account for the spent money on your budget. For this reason, whenever a credit card transaction occurs, money needs to be subtracted from the appropriate budget columns. An equal amount of money then needs to be added to the Credit Card category. This methodology insures that you will have enough money available when the credit card bill comes due, allowing you to pay it off in full each month.

The sample budget indicates that Jack and Jill had 11 credit card purchases during the first half of the month. Notice that in some cases one transaction can result in deductions from multiple columns. For instance, Jack bought $72.50 worth of food at WalMart, but also bought a magazine for $5.28. The latter is a personal item and thus is subtracted from Jack’s budget category. Of course, the amount of the total purchase, $77.78, gets added into the Credit Card column. A similar split occurs for the family’s outing to the movie theater. Based on the low cost of the tickets, it appears that they went to a matinee.

Remember that Jack and Jill are also putting an extra $250 every budget cycle into the Credit Card category in order to have extra money to pay off existing debt. Thus, when a credit card bill comes due, their total payment will be the amount of all the purchases made during the billing cycle PLUS the amount designated for paying off their existing debt. Let’s suppose that $100 was allocated for paying off their existing MasterCard debt. Further suppose that $400 in charges were made during a billing cycle. Then, the payment for that cycle will be $500.

Cash Transactions

All the money carried in an individual’s wallet should be thought of as being that person’s personal money. Therefore, if Jack pays cash for something personal, such as a book, then nothing needs to be put on the budget spreadsheet. However, if Jack pays for a snack with his cash, then he will need to be compensated for this on the budget by transferring the cost of the snack from the Food category to the Jack category. This means it is a good idea to make a note of any non-personal cash transactions to help you remember to compensate yourself on the next budget.

Since this is your first budget, you may not want to start out having a personal claim on the money in your wallets. You may have different amounts and it wouldn’t be fair starting out with one person having more money than the other. So, let’s just say that any money in your wallets at the beginning of the month is money that belongs in Savings. There is no need to actually deposit this cash into your checking account. You can simply transfer money on the spreadsheet. For our sample budget, Jack started the month with $100 in his wallet while Jill started with $25. The “Initial Cash Balancing” entry on the spreadsheet handles the compensation by transferring $100 from Jack’s column and $25 from Jill’s column to the Savings column. After doing this, all the cash in their wallets can now be considered their personal money.

How Did They Do?

So, how did Jack and Jill do? Quite well, actually. They managed to keep most of their budget categories in the black. You might thing they messed up by overspending on food. Perhaps, but another explanation could be they bought enough food this budget cycle to last through much of the next one. If this is so, we can expect them to spend less on food during the next budget cycle. However, if they did truly overspend, then they will just have to hunker down and spend less during the next budget cycle.

It also appears that both Jack and Jill severely overspent their personal money. Not so. Remember that they both started with some cash in their wallets and Jill also made a cash withdrawal. So, if Jack started with $100 in his wallet and spent only $22 for personal stuff, he would still have $78 left. He also spent $2 for a snack, leaving him with $76, but keep in mind this was reimbursed to Jack on the budget from the Food category. So, if Jack has $76 in his wallet and his budget column is left with a deficit of $59.28, he still has a net amount of $16.72 ($76 - $59.28). So, Jack is good. Jill started with $25 and withdrew an additional $40 from the bank. This gave her a total of $65. Of that, she spent $5.46 on food, $4.50 on miscellaneous items, and gave $20 in cash to charity. Of course she was reimbursed these amounts on the budget, but that still left her with less cash. $35.04 to be exact. If she spent $9.50 on personal items, she would be left with $25.54. Subtracting her budget deficit of $23.72, Jill ends up with an overall balance of $1.82. Above zero, but not quite as good as Jack’s overall balance of $16.72.

Finishing Up

Once the budget spreadsheet is complete, we recommend saving it with a filename of Budget-YYYY-##, where YYYY is the current year and ## is the budget number for that year. So, for this first budget of the year, the name would be Budget-2012-01. As more budget spreadsheets are created during the year, the last two digits will increase by one for each new budget. If you want to keep a hardcopy record of your budget sheets, then print this spreadsheet.

Once you have saved this file as Budget-2012-01, you need to prepare the sheet to accept the transactions for the next budget cycle. There are several steps you need to take.

1. Since the Ending Balance for this cycle is the Starting Balance for the next, you need to copy and paste the Ending Balance numbers to the row showing the Starting Balance. So, select cells D80 through U80, select menu item Edit/Copy, select cell D3, and then select menu item Edit/Paste Special, choosing Numbers as the method to paste. The Paste Special option is needed because the Ending Balance cells are actually formulas that add together all the cells above them. By performing a Paste Special – Numbers, the numerical results of the formulas are pasted into the Beginning Balance cells rather than the formulas themselves. Upon selecting the menu item Edit/Paste Special, OpenOffice Calc shows the following dialog box:

Excel presents something similar. In either case, the important point is that the Numbers option is the only thing selected.

2. All of the transactions for this first budget cycle need to be deleted to make way for the second budget cycle transactions. Select cells A4 through U78 and press the Delete key on your keyboard. OpenOffice Calc will show the following dialog box:

You want to delete all the content of these cells, but not the formatting since that will rid the cells of their Currency formatting.

3. Finally, you need to modify three cells. First, change cell A1 from 2012-01 to 2012-02. Next change the Starting Balance date to Jan 15 and the Ending Balance date to Jan 31. Now the sheet is ready to accept transactions for the next budget cycle and can be saved with a filename of Budget-2012-02. Here’s what it should look like.

Download Excel Version

In the next post, we’ll create some more sample transactions for the second budget cycle.

Saturday, January 7, 2012

Initializing the Spreadsheet

Now that we’ve got a budget spreadsheet built, it’s time to fill in some of the initial numbers. There are two sets of values that are needed: the Starting Balances and the Semimonthly Allowances. Let’s start with the latter since we determined these numbers in a previous post when we adjusted the category expenditures. At that time we settled on the monthly amounts for each category, whereas for the budget spreadsheet we need the semimonthly amounts. These values are simply half of the monthly amounts as can be seen in this table:

So, all that needs to be done is to enter the Modified Semimonthly numbers above into the spreadsheet on row 79 for the Semimonthly Allowances. We personally like to use even dollar amounts for our allowances, so we would round up the House Upkeep allowance to $38.

Next, we need to determine how much money to allot to each category as a Starting Balance on row 3. Actually, since you are adding money to each category twice a month, the only reason for putting any seed money into a category is that you have a regular payment due during this first budget period. Because you are just starting, you do not have any money from a previous budget in any category. So, if a monthly payment is due during this first budget period, you need seed money in order to have enough money to make the payment. For instance, suppose your $500 monthly mortgage payment is due 10 days into this first budget cycle. If you don’t put seed money into the Mortgage category, then you will only have $250 for making the payment. Thus, you need to set a Starting Balance for the Mortgage category of $250. You need to do something similar for any other budget categories where a payment is coming due soon. For the purpose of this exercise, let’s suppose you also have a utility bill, a TV cable bill, and some car insurance coming due. Also, let’s assume that you currently have $500 in your checking account. Then the Starting Balance allocations may look like this:

There seems to be a problem. You don’t have enough money in your checking account to cover the seed money needed. This means you are starting with a negative amount in the Savings category. That’s okay as long as the overall balance in your checking account stays above $0. If, however, you have too many payments coming due before you have a paycheck coming in, you might need to transfer some money from a another account to prevent an overdraft on your checking account. For our purposes here, let’s suppose your next paycheck will be deposited before any large bills are due so that no additional money is needed in your checking account. Remember too that you will be adding about $140 to the Savings category twice a month, so the $100 initial Savings deficit will go away on the first budget cycle.

Now, all that remains to be done is to enter the numbers from the above table to the Starting Balance row on the spreadsheet and resave it. It will look something like the partial view below:

Click here for image of full spreadsheet.

Click here for image of full spreadsheet.

Now you are ready to complete your first budget spreadsheet. You can download readymade copies of the initialized spreadsheet using the following links:

OpenOffice.org format (.ods):

http://www.rkaproductions.com/files/Budget Spreadsheet Initialized.ods

Excel format (.xls):

http://www.rkaproductions.com/files/Budget Spreadsheet Initialized.xls

So, all that needs to be done is to enter the Modified Semimonthly numbers above into the spreadsheet on row 79 for the Semimonthly Allowances. We personally like to use even dollar amounts for our allowances, so we would round up the House Upkeep allowance to $38.

Next, we need to determine how much money to allot to each category as a Starting Balance on row 3. Actually, since you are adding money to each category twice a month, the only reason for putting any seed money into a category is that you have a regular payment due during this first budget period. Because you are just starting, you do not have any money from a previous budget in any category. So, if a monthly payment is due during this first budget period, you need seed money in order to have enough money to make the payment. For instance, suppose your $500 monthly mortgage payment is due 10 days into this first budget cycle. If you don’t put seed money into the Mortgage category, then you will only have $250 for making the payment. Thus, you need to set a Starting Balance for the Mortgage category of $250. You need to do something similar for any other budget categories where a payment is coming due soon. For the purpose of this exercise, let’s suppose you also have a utility bill, a TV cable bill, and some car insurance coming due. Also, let’s assume that you currently have $500 in your checking account. Then the Starting Balance allocations may look like this:

There seems to be a problem. You don’t have enough money in your checking account to cover the seed money needed. This means you are starting with a negative amount in the Savings category. That’s okay as long as the overall balance in your checking account stays above $0. If, however, you have too many payments coming due before you have a paycheck coming in, you might need to transfer some money from a another account to prevent an overdraft on your checking account. For our purposes here, let’s suppose your next paycheck will be deposited before any large bills are due so that no additional money is needed in your checking account. Remember too that you will be adding about $140 to the Savings category twice a month, so the $100 initial Savings deficit will go away on the first budget cycle.

Now, all that remains to be done is to enter the numbers from the above table to the Starting Balance row on the spreadsheet and resave it. It will look something like the partial view below:

Now you are ready to complete your first budget spreadsheet. You can download readymade copies of the initialized spreadsheet using the following links:

OpenOffice.org format (.ods):

http://www.rkaproductions.com/files/Budget Spreadsheet Initialized.ods

Excel format (.xls):

http://www.rkaproductions.com/files/Budget Spreadsheet Initialized.xls

Subscribe to:

Posts (Atom)